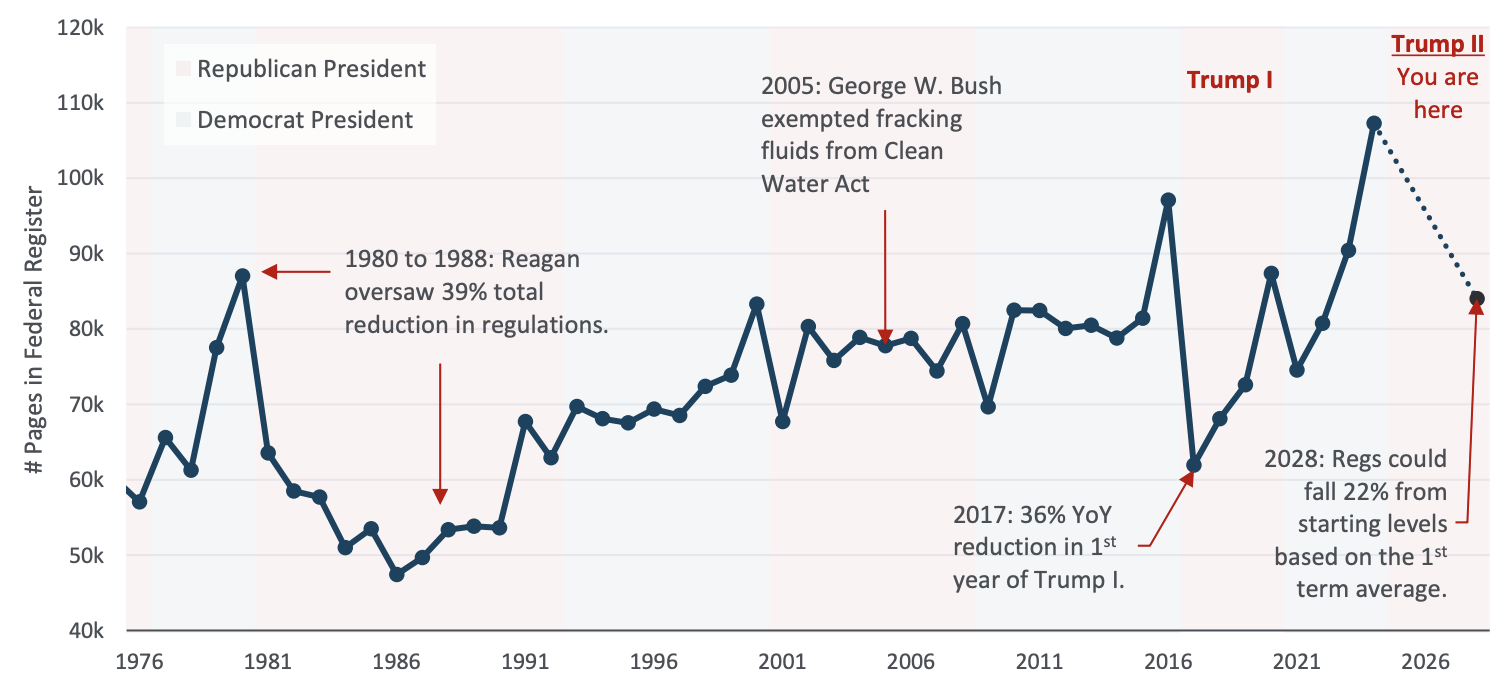

Regulations mostly decreased under Republican presidents in the modern era.

History suggests that Republican administrations often pursue deregulation, and this can influence productivity over time. For example, the Reagan administration implemented broad deregulation across multiple industries in the 1980s which spurred productivity gains emerging in the early 1990s. Similarly, the Bush administration’s exemption of fracking fluids from the Clean Water Act in 2005 helped initiate the development of the U.S. fracking industry.

During the first Trump administration, similar deregulation occurred, particularly in the energy and economic sectors. If a second term follows a comparable approach, regulation levels could decrease by 20%. While the effects may not be immediate, previous shifts have aligned with periods of higher productivity growth.

Federal Regulations as proxied by the Federal Register page count

The Federal Register, published by the National Archives, contains all rules, proposed rules, and regulations of the Federal Government. Sources:

https://www.govinfo.gov/help/fr#about, The George Washington University Regulatory Studies Center, “Total Pages Published in the Federal Register" retrieved 6/2/2025, go.gwu.edu/regstudies.

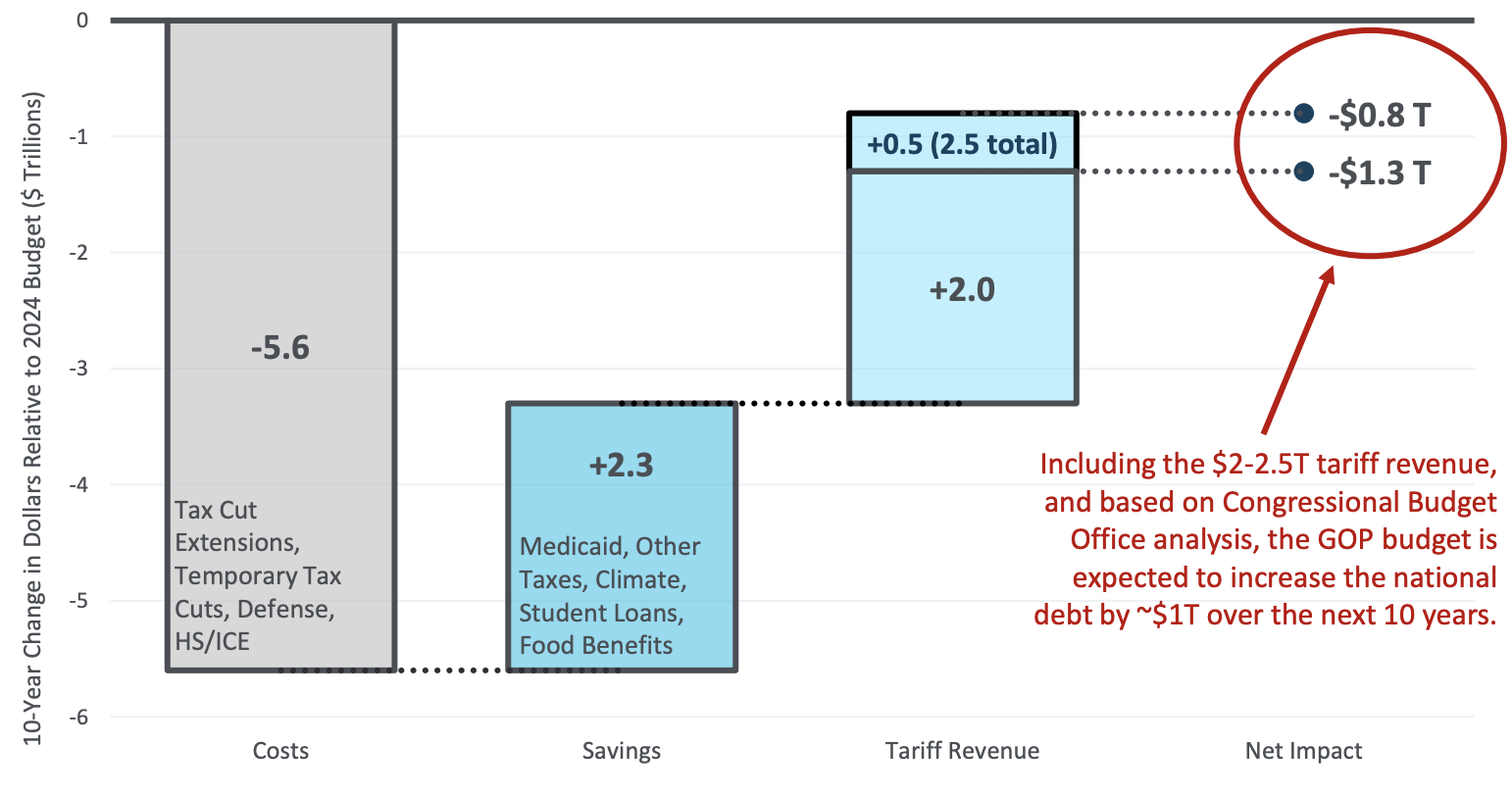

Potential tariff revenue may offset much, but not all, of 10-year debt increase.

The latest spending package – as passed initially by the House – might’ve surprised investors by potentially reducing the national debt over ten years. However, the final version has a projected cost of approximately $5.6 trillion over ten years which is only expected to be partially offset by an estimated $2.3 trillion in savings. Though not formally included in the legislative text, a proposed 10% universal tariff could generate $2 to $2.5 trillion in additional revenue. Taking these assumptions into account, the net addition to the federal debt over a decade would be around $1 trillion.

Net Effects of Trump's Fiscal Policies over Next 10 Years

Source: The Economist analysis of Congressional Budget Office data. Amounts do not include all effects of interactions between all provisions. The listed sources of costs and savings show the top 5 items from each category

Past performance does not guarantee future results. Investing in securities involves risk, including the possibility of the loss of principal.

Please see Advisory Research’s Form ADV Part 2A, which is available upon request, for more information.

Advisory Research is providing this material for informational purposes only. The information provided is not intended to recommend any company or investment described herein, and is not an offer or sale of any security or investment product or investment advice. Before making any investment decision, you should seek expert, professional advice and obtain information regarding the legal, fiscal, regulatory and foreign currency requirements for any investment according to the laws of your home country or place of residence.

Certain information contained herein constitutes forward looking statements, projections and statements of opinion (including statements of financial market trends). Such information can typically be identified by the use of terminology such as “may”, “will”, “should”, “expect”, “anticipate”, “project”, “estimate”, “intend”, “continue” or “believe” or comparable terminology. All projections, opinions and forward looking statements are based on information available to Advisory Research as of the date of this presentation, and Advisory Research’s current views and opinions, all of which are subject to change without notice. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in forward looking statements. Additionally, information and views presented herein may be drawn from third-party or public sources which are believed, but not guaranteed, to be reliable and which have not been verified for accuracy or completeness.

Advisory Research’s strategies are actively managed and not intended to replicate the performance of any cited index: the performance and volatility of Advisory Research’s investment strategies may differ materially from the performance and volatility of a cited index, and their holdings will differ significantly from the securities that comprise the index. You cannot invest directly in an index, which does not take into account trading commissions and costs.

Advisory Research is an investment adviser in Chicago, IL. Advisory Research is registered with the Securities and Exchange Commission (SEC). Registration of an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. Advisory Research only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of Advisory Research’s current written disclosure brochure filed with the SEC which discusses among other things, Advisory Research’s business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov

.jpg?width=1000&height=1000&name=Swaim%20(website).jpg)

.jpg?width=1000&height=1000&name=Harvey%20(website).jpg)

.jpg?width=1000&height=1000&name=Steffanus%20(Website).jpg)

.jpg?width=1000&height=1000&name=M.%20Valentinas%20(website).jpg)

-min.jpg?width=394&height=394&name=Zessar%20(website)-min.jpg)

-1.jpeg?width=502&height=502&name=Florida%20(website)-1.jpeg)

.jpg?width=1000&height=1000&name=Lamb%20(website).jpg)

.jpg?width=1000&height=1000&name=Prassas%20(website).jpg)

.jpg?width=1000&height=1000&name=Crawshaw%20(website).jpg)

.jpg?width=1000&height=1000&name=Clarke%20(website).jpg)

.jpg?width=1000&height=1000&name=Cialdella%20(website).jpg)

.jpg?width=1000&height=1000&name=Harmon%20(website).jpg)

.jpg?width=1000&height=1000&name=Tracy%20(Website).jpg)