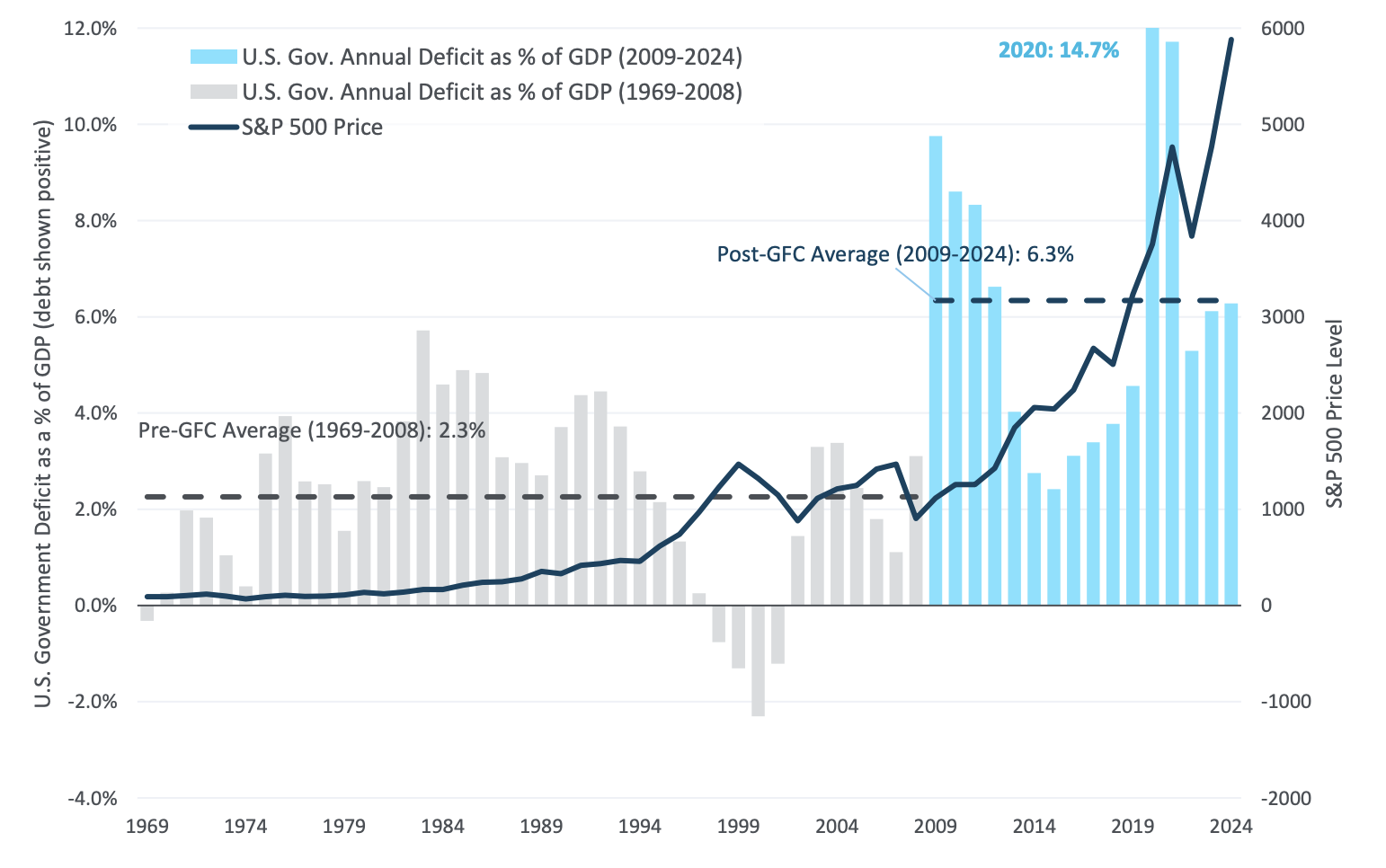

Federal deficit spending was a likely catalyst for U.S. equity markets.

We think federal deficit spending has played a significant role in supporting U.S. equities over the past 15 years. Prior to the Global Financial Crisis (GFC), federal deficits typically averaged around 2.3% of GDP. However, following the GFC and then later in response to the COVID-19 pandemic, deficits increased dramatically, coinciding with and preceding relatively extended periods of strong equity market performance. With current fiscal constraints, however, there is uncertainty about whether this level of support can continue and what implications that might have for future equity performance.

Increased Deficit Spending Helped Juice S&P 500 Performance

Source: Federal Reserve Bank of St. Louis “FRED”. Past performance is no guarantee of future results. An index is unmanaged and unavailable for direct investment.

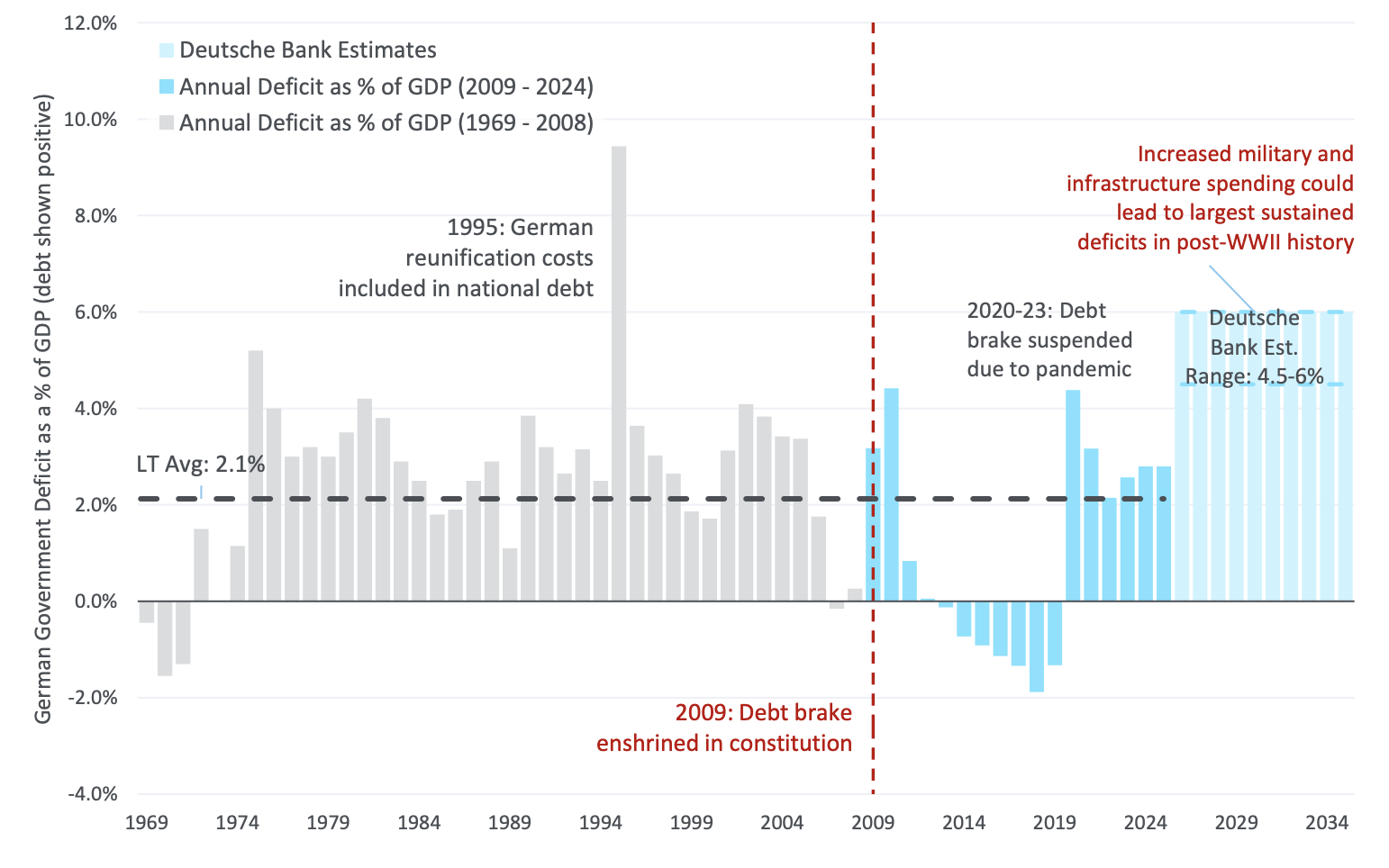

Germany set to abandon a decade of austerity in favor of fiscal excess.

In Europe, fiscal policy has followed a similar trajectory in some respects. For many years, Western-democracies maintained deficit levels near 2% of GDP in line with neoliberal economic norms. However, the eurozone crisis prompted tighter fiscal rules, most notably in Germany, where a constitutional amendment in 2009 introduced the so-called "debt brake," requiring fiscal surpluses. This rule was temporarily relaxed during the pandemic, allowing for moderate deficits.

More recently, geopolitical developments and security concerns have driven significant shifts in European fiscal policy. Germany recently amended its constitution to remove the debt brake and permit higher spending - a structural change that is expected to increase government expenditures to 5-6% of GDP split between defense and infrastructure. This marks a notable departure from previous fiscal restraint and could be a tailwind for European equities.

Is this the start of European fiscal excess?

Source: Finaeon, Eurostat, Haver Analytics, Deutsche Bank. As of March 2025.

Past performance does not guarantee future results. Investing in securities involves risk, including the possibility of the loss of principal.

Please see Advisory Research’s Form ADV Part 2A, which is available upon request, for more information.

Advisory Research is providing this material for informational purposes only. The information provided is not intended to recommend any company or investment described herein, and is not an offer or sale of any security or investment product or investment advice. Before making any investment decision, you should seek expert, professional advice and obtain information regarding the legal, fiscal, regulatory and foreign currency requirements for any investment according to the laws of your home country or place of residence.

Certain information contained herein constitutes forward looking statements, projections and statements of opinion (including statements of financial market trends). Such information can typically be identified by the use of terminology such as “may”, “will”, “should”, “expect”, “anticipate”, “project”, “estimate”, “intend”, “continue” or “believe” or comparable terminology. All projections, opinions and forward looking statements are based on information available to Advisory Research as of the date of this presentation, and Advisory Research’s current views and opinions, all of which are subject to change without notice. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in forward looking statements. Additionally, information and views presented herein may be drawn from third-party or public sources which are believed, but not guaranteed, to be reliable and which have not been verified for accuracy or completeness.

Advisory Research’s strategies are actively managed and not intended to replicate the performance of any cited index: the performance and volatility of Advisory Research’s investment strategies may differ materially from the performance and volatility of a cited index, and their holdings will differ significantly from the securities that comprise the index. You cannot invest directly in an index, which does not take into account trading commissions and costs.

Advisory Research is an investment adviser in Chicago, IL. Advisory Research is registered with the Securities and Exchange Commission (SEC). Registration of an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. Advisory Research only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of Advisory Research’s current written disclosure brochure filed with the SEC which discusses among other things, Advisory Research’s business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov

.jpg?width=1000&height=1000&name=Swaim%20(website).jpg)

.jpg?width=1000&height=1000&name=Harvey%20(website).jpg)

.jpg?width=1000&height=1000&name=Steffanus%20(Website).jpg)

.jpg?width=1000&height=1000&name=M.%20Valentinas%20(website).jpg)

-min.jpg?width=394&height=394&name=Zessar%20(website)-min.jpg)

-1.jpeg?width=502&height=502&name=Florida%20(website)-1.jpeg)

.jpg?width=1000&height=1000&name=Lamb%20(website).jpg)

.jpg?width=1000&height=1000&name=Prassas%20(website).jpg)

.jpg?width=1000&height=1000&name=Crawshaw%20(website).jpg)

.jpg?width=1000&height=1000&name=Clarke%20(website).jpg)

.jpg?width=1000&height=1000&name=Cialdella%20(website).jpg)

.jpg?width=1000&height=1000&name=Harmon%20(website).jpg)

.jpg?width=1000&height=1000&name=Tracy%20(Website).jpg)