A Late Summer Storm

Just as European bankers sat down for their Aperol Spritz in St Tropez, the markets decided to interrupt the idyllic August summer holidays. The catalyst was likely technical in nature – the unwinding of a crowded Yen carry trade combined with one bad macro print. When the fast money deleverages in a very illiquid summer market, their risk controls dictate the selling of their most liquid assets. US large cap Technology stocks - widely owned by the Hedge Fund community, extraordinarily liquid with expensive valuations – were an easy decision to sell by institutional investors. Thus, markets managed to plunge over 10% in less than a week.

A Recession is a Process not an Event

Recessions are classically identified after the fact almost as if it’s a date on the economic calendar. But a recession is not an event but a reflexive process. Instead of defining recession by contracting GDP growth, we prefer to define it by the labor market, and the timing is very dependent on when people start losing jobs. When workers start losing their jobs (or start to fear losing their jobs), confidence and spending begin to decline which eventually makes its way into corporate earnings (the main driver for stock prices).

So, the ‘Sahm Rule*’ is a convenient indicator for recession hunters as it is based on labor market conditions. The ‘Sahm Rule’ worked historically because it identifies higher unemployment due to job losses – a trigger for the reflexive recessionary process. The unemployment rate is indeed moving higher and is currently flashing red for recession. But higher unemployment is due to strong labor force growth - both increased worker participation and immigration – not workers losing their jobs. There continues to be a great deal of resilience in the service sector with increased jobs and strong wage growth.

The Fed Put is Back

Central Bankers are easy punching bags if you wear political stripes. Central Bankers wave a most powerful wand under opaque papal-smoke-like circumstances. But we believe that the Fed’s recent track record has been quite impressive. Chairman Powell did not cave to political pressure and kept monetary policy tight enough to cool inflation and store dry powder for eventual rate cuts.

The Covid supply shocks were a shock to the price level but not a permanent increase in the inflation rate. Labor is still the main driver for US inflation and the more balanced and healthy US job market will likely keep inflation contained. As the Fed slayed the inflation dragon, the Fed can now pivot to the second part of its dual mandate – maximum employment. Which means in practice that a recession is not an option and the Fed Put is back. Macro data is on a glide path. We believe that the Fed will delicately secure the soft landing via gradual rate cuts of 150-200 bps during this cycle.

Fade the Bearish Sentiment

The veritable cottage industry of bears has been calling for various forms of recessions and hard landings for months. We think that the promising economic backdrop and skillful Central Bank, are underappreciated by most equity investors who continue to wait for the other shoe to drop. We expect Central Banks to remain proactive and the economic data better than expected. We remain very bullish on Global equities. If we’ve learned one thing in a two-decade career in equities: performance tends to be better when sentiment is negative.

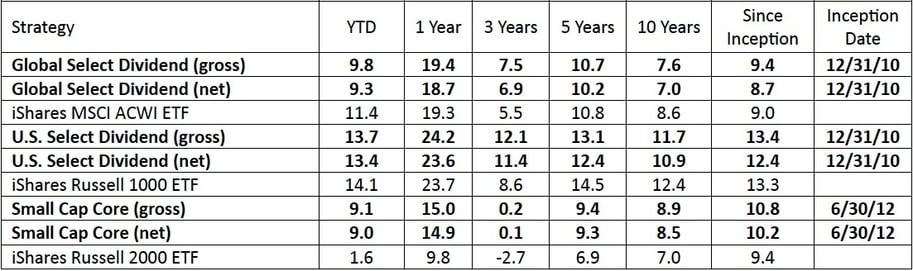

Performance Update

The Select Dividend strategies have mostly kept pace with their broad strategy benchmarks YTD. This might seem like an average result; however, it is anything but in a narrowly driven Tech market. For example, NVDA represented 3.5% of the SPX’s 15.5% 1H24 gain. The Select Dividend strategies remain in the top quartile of their peer group for the YTD period**.

Our Small Cap Core strategy has strongly performed YTD, outperforming the iShares Russell 2000 ETF by 7.4% on a net basis. Small Cap Core benefits from less index concentration - particularly in technology – allowing our disciplined investment process to capture idiosyncratic alpha.

Trailing Returns as of 6/30/2024

*The ‘Sahm Rule’ is a recession indicator that is triggered when the 3-month moving average of U.S. unemployment rate is ≥ 0.50% above the lowest 3-month moving average level across the previous 12 months.

**Advisory Research composite peer rankings represent percentile rankings which are based on the respective monthly returns and reflect where those returns fall within the indicated eVestment Alliance (EA) universe. The universe for this analysis is all Global Dividend managers in the EA universe, and ranking data is based on performance as of 6/30/24. The analysis was generated on 7/15/24 and is subject to change as additional firms within the category submit data. EA provides third party databases, including the institutional investment database from which the presented information was extracted. The EA institutional investment database consists of thousands of active institutional managers, investment consultants, plan sponsors, and other similar financial institutions actively reporting on over 10,000 products. Advisory Research pays an annual fee to eVestment to access their platform and to use their data, including peer group rankings, in marketing materials. Advisory Research does not pay specifically for the ranking.

Past performance does not guarantee future results. Investing in securities involves risk, including the possibility of the loss of principal.

Gross performance is shown net of all trading costs/commissions and gross of all management fees. Net performance is shown net of all trading costs/commissions and management fees. Unless otherwise stated, performance greater than one year is annualized. Actual client portfolio results may differ, based on, among other things, an account’s particular investment objectives and restrictions, asset levels, and timing of contributions and withdrawals.

Please see Advisory Research’s Form ADV Part 2A, which is available upon request, for more information.

Certain information contained herein constitutes forward looking statements, projections and statements of opinion (including statements of financial market trends). Such information can typically be identified by the use of terminology such as “may”, “will”, “should”, “expect”, “anticipate”, “project”, “estimate”, “intend”, “continue” or “believe” or comparable terminology. All projections, opinions and forward-looking statements are based on information available to Advisory Research as of the date of this presentation, and Advisory Research’s current views and opinions, all of which are subject to change without notice. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in forward looking statements. Additionally, information and views presented herein may be drawn from third-party or public sources which are believed, but not guaranteed, to be reliable and which have not been verified for accuracy or completeness.

Advisory Research is providing this material for informational purposes only. The information provided is not intended to recommend any company or investment described herein and is not an offer or sale of any security or investment product or investment advice. Before making any investment decision, you should seek expert, professional advice and obtain information regarding the legal, fiscal, regulatory, and foreign currency requirements for any investment according to the laws of your home country or place of residence.

Benchmark comparison is presented using the iShares MSCI ACWI ETF, iShares Russell 1000 ETF, and the iShares Russell 2000 ETF as Advisory Research considers these ETFs to parallel both associated risk and the investment style presented by each strategy.

The iShares MSCI ACWI ETF seeks to track the investment results of an index composed of large and mid-capitalization developed and emerging market equities. The iShares Russell 1000 ETF seeks to track the investment results of an index comprised of large- and mid-capitalization U.S. equities. The iShares Russell 2000 ETF seeks to track the investment results of an index composed of small-capitalization U.S. equities.

Advisory Research’s strategies are actively managed and not intended to replicate the performance of any cited index: the performance and volatility of Advisory Research’s investment strategies may differ materially from the performance and volatility of a cited index, and their holdings will differ significantly from the securities that comprise the index. You cannot invest directly in an index, which does not take into account trading commissions and costs.

Advisory Research is an investment adviser in Chicago, IL. Advisory Research is registered with the Securities and Exchange Commission (SEC). Registration of an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. Advisory Research only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of Advisory Research’s current written disclosure brochure filed with the SEC which discusses among other things, Advisory Research’s business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov.

.jpg?width=1000&height=1000&name=Swaim%20(website).jpg)

.jpg?width=1000&height=1000&name=Harvey%20(website).jpg)

.jpg?width=1000&height=1000&name=Steffanus%20(Website).jpg)

.jpg?width=1000&height=1000&name=M.%20Valentinas%20(website).jpg)

-min.jpg?width=394&height=394&name=Zessar%20(website)-min.jpg)

-1.jpeg?width=502&height=502&name=Florida%20(website)-1.jpeg)

.jpg?width=1000&height=1000&name=Lamb%20(website).jpg)

.jpg?width=1000&height=1000&name=Prassas%20(website).jpg)

.jpg?width=1000&height=1000&name=Crawshaw%20(website).jpg)

.jpg?width=1000&height=1000&name=Clarke%20(website).jpg)

.jpg?width=1000&height=1000&name=Cialdella%20(website).jpg)

.jpg?width=1000&height=1000&name=Harmon%20(website).jpg)

.jpg?width=1000&height=1000&name=Tracy%20(Website).jpg)